Categories: Tech Magazines

Unlocking Potential Goldman Sachs Embraces Blockchain

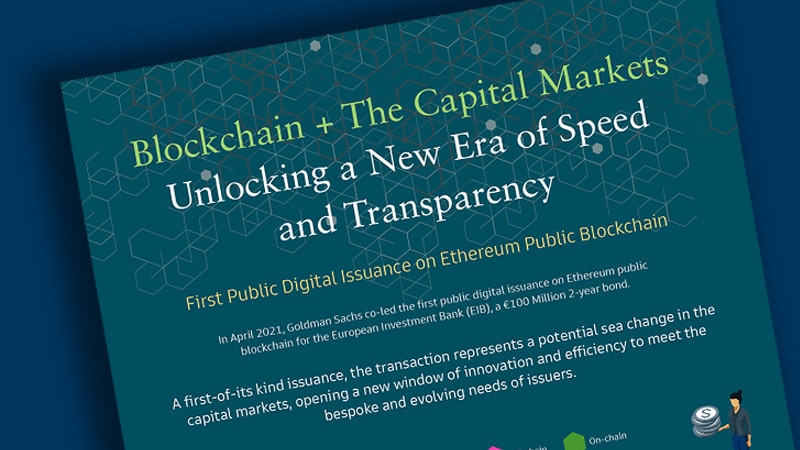

Unlocking Potential: Goldman Sachs Embraces Blockchain

In the fast-paced world of finance, adaptation is key to survival. And one of the most significant adaptations in recent times is the integration of blockchain technology. Goldman Sachs, a global leader in investment banking and financial services, has been quick to recognize the potential of blockchain and has embarked on a journey to embrace this revolutionary technology.

Understanding the Landscape

Before delving into Goldman Sachs’ foray into blockchain, it’s essential to understand the landscape of this transformative technology. Blockchain, at its core, is a decentralized digital ledger that records transactions across multiple computers